So, you’ve been hearing a lot about cryptocurrency, maybe even dipping your toes in. It’s exciting stuff, right? But then tax season rolls around, and you start wondering, ‘How Is Crypto Taxed?’ It can feel a bit confusing, especially when the places you bought your crypto from don’t seem to have all the answers. Let’s break down what you need to know about your crypto tax obligations and what might not be so clear from the exchanges.

Key Takeaways

- Yes, you generally have to pay taxes on crypto; it’s not like its tax-free money. When you sell or trade it that usually counts as a taxable event leading to capital gains or losses.

- Earning crypto through things like mining, staking, or getting airdrops is typically seen as income, so you’ll owe taxes on that too. Keeping good records of everything you do with crypto is super important for accurate reporting.

- The way your crypto is taxed really depends on what you actually do with it. Exchanges often can’t give you perfect tax forms because they don’t see the whole picture of your transactions, especially if you move crypto around a lot.

When Crypto Transactions Become Taxable Events

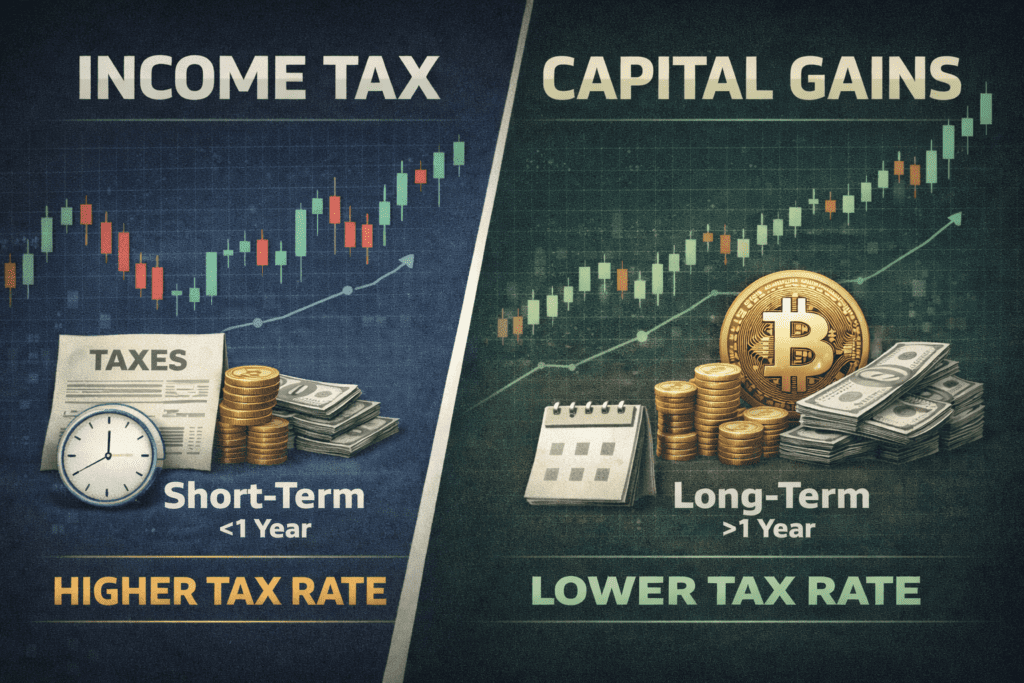

Generally, you have to pay taxes on crypto when you dispose of it. This means selling it for fiat currency (like Canadian dollars), trading it for another cryptocurrency, or using it to buy goods or services. Each of these actions is considered a disposition, and it’s where the tax clock starts ticking. The key is to track these events meticulously.

Here’s a breakdown of common taxable events:

- Selling Crypto: When you sell your Bitcoin for CAD, that’s a taxable event.

- Trading Crypto: Swapping Ethereum for Litecoin? That’s also a taxable event.

- Spending Crypto: Using your crypto to buy a coffee or a new gadget counts.

- Receiving Crypto as Payment: If you’re paid in crypto for goods or services, it’s income.

It’s not just about selling for a profit, either. Even if you sell crypto at a loss, that’s still a taxable event, and you’ll need to report it. This is important for potentially offsetting other gains you might have. Understanding these basics is a solid first step towards managing your crypto tax obligations [fce8].

The CRA treats cryptocurrency much like other assets, such as stocks or commodities. This means that your crypto activities can result in either capital gains or business income, depending on the nature of your transactions.

Income Earned Through Cryptocurrency

Beyond just buying and selling, you can earn cryptocurrency in various ways, and most of these are also taxable. If you’re mining new coins, receiving them through an airdrop, or earning rewards from staking your existing crypto, the CRA considers this income. The amount of income is generally the fair market value of the cryptocurrency in Canadian dollars at the time you receive it.

For example, if you receive 0.1 ETH from staking rewards, and at that exact moment, 0.1 ETH is worth $300 CAD, then you’ve earned $300 in income. This income is then added to your cost basis for that specific crypto, which will be relevant when you eventually sell or trade it.

- Mining: Earning new coins through the process of mining.

- Staking: Receiving rewards for holding and validating crypto transactions.

- Airdrops: Getting free tokens, often as a promotion or part of a new project launch.

- Interest: Earning interest on crypto held in certain accounts or platforms.

Keeping track of all these different income streams is vital for accurate tax reporting. It might seem like a lot to manage, but getting a handle on it early will save you a lot of headaches down the road.

Navigating Crypto Tax Reporting Challenges

Dealing with crypto taxes can feel like trying to solve a puzzle with missing pieces, especially when you’re trying to get your tax forms in order. Exchanges often don’t make it easy, and figuring out your cost basis can be a real headache. Let’s break down why this happens and what you can do about it.

Why Exchanges Struggle to Provide Accurate Tax Forms

It’s a common frustration: you expect your crypto exchange to hand over a neat tax form, but what you get is often incomplete or just plain confusing. There are a few big reasons for this. First, exchanges operate globally, and tax laws vary wildly from country to country, and even state to state. They have to build systems that try to account for all these different rules, which is incredibly complex. Second, many exchanges don’t track your cost basis – that’s what you originally paid for your crypto, including fees. They might show you your sales, but not necessarily what you need to calculate your profit or loss accurately for tax purposes. This means the responsibility often falls squarely on your shoulders. You might get a transaction history, but turning that into a tax report is a whole different ballgame.

Methods for Tracking Your Crypto Cost Basis

Since exchanges aren’t always helpful, you need a plan for tracking your cost basis yourself. This is super important because it directly affects how much taxable gain or loss you report. Here are a few ways to tackle it:

- Manual Spreadsheets: This is the most basic method. You’ll need to record every single transaction: the date, the type (buy, sell, trade and gift), the crypto involved, the quantity, and the value in USD (or your local currency) at the time of the transaction. You’ll also need to track any fees paid. It’s time-consuming, especially if you have many transactions, but it gives you complete control.

- Crypto Tax Software: There are many software tools designed specifically for this. They can often connect directly to your exchange accounts and wallets via APIs to automatically import your transaction data. These tools then help calculate your cost basis and generate tax reports. Look for software that supports all the platforms you use and offers features like capital gains calculation and different accounting methods (like FIFO or LIFO, if applicable in your jurisdiction).

- Hiring a Professional: If your crypto activity is extensive, involves complex transactions like DeFi or NFTs, or you’re just not comfortable managing it yourself, a tax professional specializing in cryptocurrency can be a lifesaver. They have the tools and knowledge to sort through your records and ensure everything is reported correctly.

Tax Implications of Lost or Stolen Cryptocurrency

Losing access to your crypto, whether due to a hack, a lost private key, or a scam, can feel like a total loss. From a tax perspective, it’s a bit more complicated. Generally, if your cryptocurrency is stolen, you might be able to claim a capital loss. This is only possible if you can prove the theft and that you took reasonable steps to secure your assets. Think of it like losing a physical asset; if it’s gone and you can’t get it back, it might be deductible. However, you’ll need documentation to support your claim. This could include police reports, exchange notifications, or any communication related to the loss. Without proof, the IRS might not recognize it as a deductible loss. It’s a good idea to keep records of your security measures, like hardware wallets or multi-factor authentication, to show you acted responsibly.

Tax Treatment of DeFi and Staking Rewards

Getting into Decentralized Finance (DeFi) or staking your crypto can feel like earning passive income, and in many ways, it is. But it also comes with tax obligations. When you earn rewards from staking, lending, or providing liquidity in DeFi protocols, these rewards are typically considered taxable income. You’ll need to report the fair market value of the crypto you receive as income at the time you receive it. This means keeping track of the value of those rewards on the day they hit your wallet. Later, when you decide to sell or trade these rewards, any profit or loss will be treated as a capital gain or loss, based on the difference between your cost basis and the sale price. This can get complicated quickly, especially with automated strategies that might generate many small transactions. It’s important to track the cost basis of these rewards accurately from the moment you receive them. For many, using specialized crypto tax software or a detailed spreadsheet is the best way to manage these complex transactions and ensure you’re reporting everything correctly. If you’re unsure about how to handle these types of income, consulting with a tax professional who understands digital assets is a smart move. They can help you understand how to report these earnings and calculate your capital gains or losses accurately, especially when dealing with various types of crypto transactions.

Wrapping Up Your Crypto Taxes

So, you’ve seen that dealing with crypto taxes isn’t exactly straightforward. Exchanges often can’t give you the full picture for your tax forms because of how crypto moves around. This means you’re likely going to need to keep your own detailed records, whether that’s with a spreadsheet or some software. Remember, holding, transferring between your own wallets, or gifting crypto below a certain amount might not be taxable events right away, but earning it through mining or staking usually is. When you sell or trade, that’s when capital gains or losses come into play. The IRS is getting better at tracking this stuff, so it’s really in your best interest to get your records in order now. Don’t wait until tax season to figure it all out; start tracking your transactions today.